This article focuses on personal insurance, how and what you need to look out for as well as our top tips in looking for an insurance policy.

Dead Money – The cornerstone of good financial planning?

I‘ve advised many clients over the years and the fact remains that whilst the single most important product that anyone can ever buy is insurance, this is one thing that clients don’t have and most often, have not considered. There is a feeling that insurance premiums are ‘dead money’. It is a catch 22 situation, there is a feeling that you are paying for something that you haven’t used or when you do use it, you have suffered an illness or traumatic event and it isn’t a pleasant experience.

What you do get in purchasing insurance, is peace of mind. Knowing that your family is protected in the event that you are unable to contribute financially alleviates stress and allows you to focus on spending carefree time with your family.

It’s all about income

Almost all of our aspirations, hopes and dreams pivot around our ability to produce an income. This includes the home you own, the university your children go to, the clothes you wear and the food you eat and in some cases, even the number of children you have.

Regardless of whether you are considering life insurance, trauma, disability or income protection, these insurance products are primarily there to provide a regular income or a lump sum that your family can use to provide an income to you or in the event of your death. This ensures that your family can continue with the same lifestyle.

In our first Focus on life insurance, we look at insurance in its various forms, pure life insurance, trauma, disability and income protection.

In our first Focus on life insurance, we look at insurance in its various forms, pure life insurance, trauma, disability and income protection.

Life insurance is by no means a modern invention. Some 2000 years ago, in Roman times, a form of life insurance was practised by burial societies. These societies paid the funeral costs of members out of monthly payments to the societies.

Similar organisations sprang up in the Middle Ages in Britain as Trade Guilds tried to provide for the funeral costs of members. These early societies and guilds had no data on which to base their calculations, civilisation had not yet developed to the extent of recording births and deaths and there was no real idea of how long people were expected to live for. It was only in 1582 that any effort was made to start collecting records of baptisms and burials which then led to the structuring of mortality tables and costing of premiums as we know it today. In its simplest form – the older you are the more likely you are to die.

Unlike most products that you purchase in our “buy now, pay later” economy, financial products, and in particular, insurance, require you to pay now and reap the benefit later. You are in effect, putting your faith into an insurance company to pay you in your times of need.

In this vein, our focus on life insurance is designed to give you a greater understanding in how insurance products work, how you can calculate how much cover you need and some simple steps to ensure you get the best value insurance product.

Driving the cost of insurance

Whilst calculating how much insurance should cost you, there are a huge number of factors that drive the cost of the underlying insurance:

- Age – The older you are the more likely you are to die, and as a result the older you are the more its going to cost.

- Sex – Women live approximately five years longer than men and whilst this makes it cheaper for them to look at life insurance, they’re more complex anatomy means that they suffer more illnesses, making it more costly for health based insurances.

- Health – One of the primary drivers in determining the cost of life insurance is your health. Insurers look to protect the pool of policyholders by loading premiums for new applicants with poorer health and in some instances will even refuse cover altogether.

- Smoking – In most cases smokers will pay a hefty loading due to the associated additional illnesses and their shorter life expectancy.

- Occupation – This is a primary driver of cost when looking at Income Protection but can also impact on the rates for life, trauma and disability cover. So, higher risk or higher skilled occupations such as firemen or surgeons have a higher cost associated with their cover.

Other additional factors that are not as obvious but will nevertheless influence the underlying rate include, where you live, your occupation, lifestyle, the overall level of commission paid to a sales intermediary as well as the underlying profitability of the company.

How much is enough?

Whether you’re considering life, trauma, income protection or TPD insurance, if you are the breadwinner, you will want to keep your family in the style to which they have become accustomed. If you’re a housewife/househusband, then you will need to provide money for someone to do the things you did if you’re not around or incapacitated. Consider this

- How much money might be needed in order to pay off your debts such as your mortgage or personal loans?

- How much money do your dependents need to continue to live in the same lifestyle they currently enjoy?

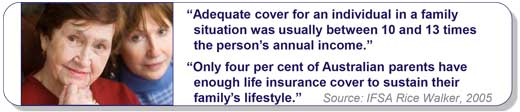

Life Insurance – As an approximate rule of thumb, you should consider insuring yourself for 10 times your salary.

Trauma, Disability and Income Protection – When insuring yourself for trauma, disability or income protection you should aim to produce around two thirds of your earnings or a minimum of $50,000 indexed for inflation.

- How much can you afford to pay?

You get what you pay for

For many, cost is the primary consideration. It’s a question of affordability versus what you need.

Ultimately, how much cover you and your family needs will vary from household to household, so it’s up to you to decide how much money should leave your family with a reasonable standard of living.

A better question when considering how much insurance to take out is ‘How much cover can I afford?’

One thing is clear:

Unless you have accumulated so much wealth that you can afford not to work tomorrow, you have a need to insure yourself and your family.

Quote & apply with Zurich in 5 mins

Our online portal with Zurich Ezicover contains a quick calculator allowing you to quote and apply online.

If you are unsure as to how much cover you need, Zurich’s quick calc can also help you work out what may be the best level of cover for your needs. Alternatively, if you just want to see what you can get for X dollars a month, Zurich’s quick calculator will give you an immediate quote.

When it comes to insuring yourself & family, something is always better than nothing

Comment: